HSAs in 2026: Maximize Tax Benefits for Medical Expenses

Healthcare Savings Accounts (HSAs) in 2026 provide unparalleled triple tax advantages for eligible individuals, allowing tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses, making them a crucial tool for financial wellness.

Navigating the complexities of healthcare costs and personal finance can be daunting, but understanding tools like Healthcare Savings Accounts (HSAs) in 2026: Maximizing Tax Benefits for Medical Expenses can significantly ease the burden. These powerful accounts offer a unique opportunity to save for future medical needs while enjoying substantial tax advantages, a benefit increasingly vital in today’s economic landscape.

Understanding HSA Fundamentals for 2026

Healthcare Savings Accounts (HSAs) are far more than just savings vehicles; they are a cornerstone of savvy financial planning for healthcare. In 2026, their relevance continues to grow as medical costs steadily increase, making their tax-advantaged structure particularly appealing. An HSA functions as a personal savings account where individuals can deposit funds to cover qualified medical expenses, from doctor visits and prescriptions to dental and vision care.

The core eligibility requirement for opening and contributing to an HSA is enrollment in a High Deductible Health Plan (HDHP). These plans typically feature lower monthly premiums but higher deductibles, meaning you pay more out-of-pocket before your insurance coverage kicks in. This pairing is intentional, as the HSA acts as a buffer, allowing you to save and pay for those initial expenses with pre-tax dollars. Understanding this fundamental link between an HDHP and an HSA is the first step toward unlocking its full potential.

Furthermore, HSAs are unique in that the funds belong to you, the individual, not your employer or insurance company. This portability means the account stays with you even if you change jobs or health plans. There’s no “use it or lose it” rule; any unused funds roll over year after year, accumulating and growing over time. This long-term accumulation is a significant advantage, differentiating HSAs from Flexible Spending Accounts (FSAs).

Key HSA Eligibility Criteria

To be eligible for an HSA in 2026, several criteria must be met, primarily centered around your health insurance coverage. Adhering to these rules is crucial to avoid penalties and fully leverage the benefits.

- High Deductible Health Plan (HDHP) Enrollment: You must be covered by an HDHP, meeting specific deductible and out-of-pocket maximum thresholds set by the IRS for 2026.

- No Other Health Coverage: Generally, you cannot be covered by any other health plan that is not an HDHP, with some exceptions like vision, dental, disability, or long-term care insurance.

- Not Enrolled in Medicare: Individuals enrolled in Medicare are not eligible to contribute to an HSA.

- Not Claimed as a Dependent: You cannot be claimed as a dependent on someone else’s tax return.

Meeting these eligibility requirements ensures you can legally contribute to and benefit from an HSA. It’s always wise to confirm your specific situation with a tax professional or your health plan administrator, especially as IRS rules can have nuanced interpretations.

In essence, an HSA is a powerful financial tool designed to empower individuals with more control over their healthcare spending and savings. By combining an HDHP with an HSA, individuals can strategically manage their medical costs, save for future needs, and enjoy significant tax advantages that contribute to their overall financial well-being.

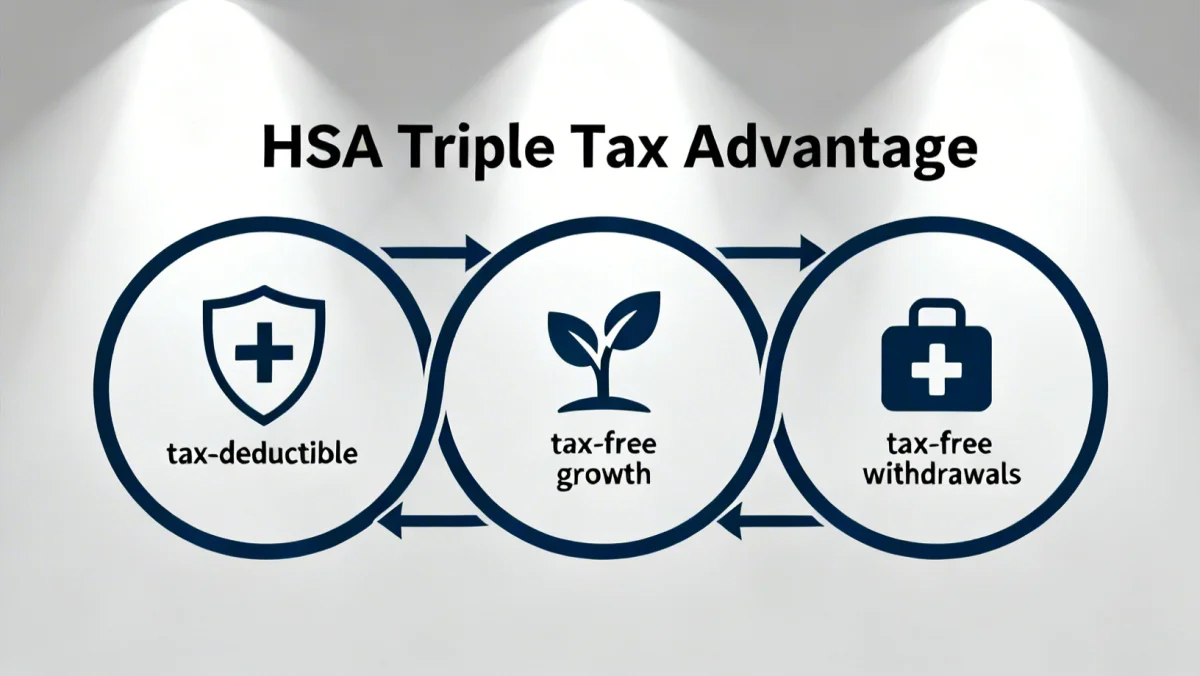

The Triple Tax Advantage: A Closer Look

The allure of Healthcare Savings Accounts (HSAs) in 2026 largely stems from their unparalleled “triple tax advantage.” This unique combination of tax benefits sets HSAs apart from nearly every other savings or investment vehicle available, making them incredibly powerful for both immediate healthcare costs and long-term financial planning.

First, contributions to an HSA are tax-deductible. This means that any money you put into your HSA reduces your taxable income for the year, potentially lowering your overall tax bill. Whether you contribute directly from your paycheck or make personal contributions, these amounts are deducted “above the line” on your tax return, even if you don’t itemize deductions. This immediate tax savings is a significant incentive for many to fund their HSA generously.

Second, the funds within an HSA grow tax-free. Once your contributions are in the account, they can often be invested, much like a 401(k) or IRA. Any interest, dividends, or capital gains earned on these investments are not taxed as long as they remain within the HSA. This tax-free growth allows your money to compound more rapidly over time, building a substantial nest egg for future medical expenses, especially as you approach retirement.

Third, qualified withdrawals from an HSA are also tax-free. When you use your HSA funds to pay for eligible medical expenses, the money you withdraw is not subject to income tax. This is where the true power of the triple tax advantage becomes evident: you get a tax break going in, tax-free growth while it’s invested, and tax-free withdrawals when you use it for healthcare. This makes HSAs an incredibly efficient way to pay for medical costs.

Understanding Qualified Medical Expenses

To ensure your withdrawals remain tax-free, it’s essential to understand what constitutes a “qualified medical expense.” The IRS defines these broadly, covering a wide range of healthcare services and products.

- Doctor Visits and Hospital Stays: This includes co-pays, deductibles, and other out-of-pocket costs for medical care.

- Prescription Medications: Most prescription drugs and certain over-the-counter medications with a doctor’s prescription are covered.

- Dental and Vision Care: Expenses for dental cleanings, fillings, braces, eye exams, glasses, and contact lenses are typically eligible.

- Therapies and Treatments: Physical therapy, chiropractic care, and mental health services often qualify.

- Medical Equipment: Items like crutches, wheelchairs, and even certain diagnostic tools may be covered.

It’s important to keep detailed records of all medical expenses, as you may need to prove to the IRS that your withdrawals were for qualified purposes. Using HSA funds for non-qualified expenses before age 65 will result in the withdrawal being taxed as ordinary income, plus a 20% penalty. After age 65, non-qualified withdrawals are taxed as ordinary income but without the penalty, effectively turning your HSA into a supplementary retirement account.

The triple tax advantage of HSAs represents a powerful financial tool for individuals and families. By maximizing contributions and strategically managing withdrawals, account holders can significantly reduce their healthcare burden and build substantial wealth over time, making HSAs a cornerstone of smart financial planning in 2026 and beyond.

Contribution Limits and Strategies for 2026

Maximizing the benefits of your Healthcare Savings Account (HSA) in 2026 requires a clear understanding of the annual contribution limits set by the IRS and strategic approaches to meet or even exceed these limits through smart planning. These limits are adjusted annually for inflation, so staying informed is crucial for effective saving.

For 2026, the IRS typically sets separate contribution limits for individuals and families. Additionally, if you are age 55 or older, you are usually allowed to make an extra “catch-up” contribution beyond the standard limit. These limits are the maximum amount that can be contributed to your HSA from all sources, including contributions from yourself, your employer, or any third party.

Strategic contributions are key. Many individuals opt to contribute the maximum allowed each year to fully leverage the triple tax advantage. Contributing regularly, perhaps through payroll deductions, can make reaching the maximum limit more manageable throughout the year. This approach also allows your funds to start growing tax-free sooner, compounding over a longer period.

Optimizing Your HSA Contributions

Several strategies can help you maximize your HSA contributions and, consequently, your tax benefits.

- Automate Contributions: Set up automatic transfers from your bank account or through payroll deductions to ensure consistent contributions without active management.

- Catch-Up Contributions: If you are 55 or older, take full advantage of the additional catch-up contribution. This extra amount can significantly boost your savings for retirement healthcare costs.

- Employer Contributions: If your employer offers contributions to your HSA, consider this part of your overall compensation package. These contributions also count towards your annual limit.

- Year-End Lump Sum: If you haven’t maxed out your contributions throughout the year, consider a lump-sum contribution before the tax filing deadline (typically April 15th of the following year) to reach the annual limit.

Remember that even if you don’t have immediate medical expenses, contributing to your HSA is still beneficial. The funds can be invested and grow, becoming a powerful retirement savings tool. Many treat their HSA as a long-term investment, paying for current medical expenses out-of-pocket and allowing their HSA funds to accumulate.

Understanding and strategically utilizing the contribution limits for your HSA in 2026 is critical for maximizing its tax benefits. By consistently contributing up to the annual maximum, and leveraging catch-up contributions when eligible, you can build a robust fund for both immediate and future medical expenses, all while enjoying significant tax savings.

Investing HSA Funds for Long-Term Growth

One of the most powerful, yet often underutilized, features of Healthcare Savings Accounts (HSAs) in 2026 is the ability to invest the funds for long-term growth. Unlike typical savings accounts, many HSAs offer investment options similar to those found in 401(k)s or IRAs. This allows your contributions to grow tax-free over decades, potentially creating a substantial nest egg for future medical expenses, especially in retirement.

The strategy here is simple: treat your HSA not just as a spending account for immediate medical needs, but as a long-term investment vehicle. By investing the money you won’t need for immediate expenses, you can take advantage of compound interest and market growth, significantly increasing the value of your account. This is particularly appealing for younger individuals who have many years until retirement, allowing their HSA balance to potentially grow into six figures or more.

Most HSA providers offer a range of investment choices, from low-risk options like money market funds to more aggressive choices such as mutual funds and exchange-traded funds (ETFs). The key is to choose investments that align with your risk tolerance and your time horizon for needing the funds. If you anticipate needing the money in the near future, more conservative investments might be appropriate. For long-term growth, a diversified portfolio of stocks and bonds is often recommended.

Developing an HSA Investment Strategy

Crafting an effective investment strategy for your HSA involves several considerations to maximize its growth potential.

- Choose a Reputable HSA Provider: Look for providers that offer a wide array of investment options, low fees, and user-friendly platforms.

- Understand Your Risk Tolerance: Determine how much risk you are comfortable taking with your investments, balancing potential returns with potential losses.

- Diversify Your Portfolio: Spread your investments across different asset classes (stocks, bonds, mutual funds) to mitigate risk.

- Regularly Review and Rebalance: Periodically check your investment performance and adjust your portfolio as needed to stay aligned with your financial goals and risk tolerance.

The beauty of investing HSA funds is that all growth is tax-free, and withdrawals for qualified medical expenses are also tax-free. This makes it an incredibly efficient way to save for retirement healthcare costs, which can be substantial. For those who can afford to pay for current medical expenses out-of-pocket, allowing their HSA to grow untouched is a highly effective strategy.

By actively investing your HSA funds, you transform it from a simple savings account into a powerful wealth-building tool. This long-term approach to your Healthcare Savings Account in 2026 can significantly enhance your financial security, ensuring you are well-prepared for both expected and unexpected medical expenses in the future.

HSA vs. FSA: Key Differences and Benefits

While both Healthcare Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) are designed to help with medical expenses, they operate under distinct rules and offer different advantages. Understanding these differences is crucial for making informed decisions about which account, or combination of accounts, best suits your financial and healthcare situation in 2026.

The most fundamental difference lies in eligibility. As previously discussed, an HSA requires enrollment in a High Deductible Health Plan (HDHP). In contrast, an FSA can typically be offered alongside any type of health insurance plan, including traditional PPO plans, as long as your employer offers it. This broader eligibility for FSAs makes them accessible to a wider range of employees.

Another significant distinction is ownership and portability. HSA funds are owned by the individual and are fully portable, meaning they stay with you even if you change employers or health plans. FSA funds, however, are generally employer-owned and are typically forfeited if not used by the end of the plan year (though some plans offer a grace period or a limited carryover amount). This “use it or lose it” rule is a major drawback for FSAs compared to the rollover feature of HSAs.

Tax advantages also differ. HSAs offer the triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. FSAs only offer two tax advantages: contributions are made with pre-tax dollars (reducing taxable income), and withdrawals for qualified medical expenses are tax-free. FSA funds cannot be invested for growth.

Choosing the Right Account for You

Deciding between an HSA and an FSA, or even using both if eligible, depends on your specific circumstances.

- HSA Advantages:

- Triple tax advantage.

- Funds roll over year to year.

- Funds are portable.

- Can be invested for long-term growth.

- Becomes a retirement savings vehicle after age 65.

- FSA Advantages:

- No HDHP requirement.

- Funds are available at the beginning of the plan year (you can use the full elected amount before contributing it all).

- Covers a wide range of qualified medical expenses.

For individuals enrolled in an HDHP, an HSA is almost always the superior choice due to its long-term investment potential and portability. If you are not eligible for an HSA, an FSA can still be a valuable tool for saving on taxes for predictable medical expenses within a given year. Some employers offer both, and if you have an HDHP, you might be able to contribute to a “limited purpose” FSA for dental and vision expenses while still contributing to your HSA for general medical costs.

Ultimately, the choice between an HSA and an FSA in 2026 hinges on your health plan, your anticipated medical expenses, and your long-term financial goals. Understanding their unique features allows you to strategically manage your healthcare finances and maximize your tax savings effectively.

Strategic Uses of HSAs Beyond Basic Medical Expenses

While Healthcare Savings Accounts (HSAs) are primarily known for covering current medical expenses, their strategic utility in 2026 extends far beyond that. For those who can afford to pay for day-to-day medical costs out-of-pocket, HSAs transform into powerful long-term savings and retirement planning tools, leveraging their unique tax advantages to build significant wealth.

One of the most compelling strategic uses is as a supplemental retirement account. After age 65, HSA withdrawals for non-qualified expenses are treated as ordinary income, similar to a traditional IRA or 401(k), but without the 20% penalty. This means that if you’ve accumulated a substantial balance by retirement, you can use those funds for anything you wish, providing a flexible source of income in your golden years. However, if used for qualified medical expenses, they remain tax-free.

Another advanced strategy involves paying for current medical expenses out-of-pocket and meticulously saving all receipts. Then, decades later, you can reimburse yourself from your HSA for those past qualified expenses, essentially creating a tax-free personal loan. This allows your HSA funds to grow untouched for as long as possible, maximizing the tax-free investment growth.

Planning for Future Healthcare Costs in Retirement

Healthcare costs in retirement can be astronomical, and an HSA is arguably one of the best tools to prepare for them.

- Medicare Premiums: HSA funds can be used to pay for Medicare Part B and Part D premiums, as well as Medicare Advantage plan premiums.

- Long-Term Care Insurance Premiums: A portion of qualified long-term care insurance premiums, based on age, can be paid with HSA funds.

- Future Medical Expenses: Even after Medicare, there will be deductibles, co-pays, and services not fully covered. An HSA provides a dedicated, tax-free fund for these costs.

- Dental and Vision Care: These often remain out-of-pocket expenses for retirees, and HSA funds can cover them.

By diligently contributing to and investing your HSA throughout your working years, you can build a robust fund specifically earmarked for these inevitable expenses. This ensures that your retirement savings in 401(k)s and IRAs are not depleted by healthcare costs, allowing them to stretch further.

The strategic deployment of Healthcare Savings Accounts in 2026 positions them as more than just a medical expense account. They are a versatile financial instrument capable of providing significant tax relief, investment growth, and robust support for both immediate and long-term healthcare needs, especially during retirement. Understanding these advanced uses can unlock even greater financial security.

Navigating Changes and Maximizing Benefits in 2026

The landscape of healthcare and finance is constantly evolving, and staying informed about potential changes to Healthcare Savings Accounts (HSAs) in 2026 is key to maximizing their benefits. While the core structure of HSAs remains stable, annual adjustments to contribution limits, deductible thresholds for HDHPs, and eligible expenses can impact how you utilize these accounts effectively.

It’s vital to regularly check for IRS announcements regarding HSA limits for the upcoming year. These adjustments typically reflect inflation and can influence your contribution strategy. For instance, an increase in the individual or family contribution limit means you have a greater opportunity to save more tax-advantaged dollars. Similarly, changes to HDHP deductible and out-of-pocket maximums will determine eligibility for new plans or continued eligibility for existing ones.

Beyond federal regulations, individual HSA providers may also introduce new investment options, fee structures, or digital tools. Regularly reviewing your provider’s offerings can ensure you are getting the most competitive rates, the best investment choices, and the most convenient access to your funds. A proactive approach to managing your HSA is essential for sustained financial health.

Tips for Ongoing HSA Optimization

To ensure you are continually maximizing your HSA benefits, consider these ongoing optimization tips:

- Stay Updated on IRS Guidelines: Periodically review IRS publications or consult a tax advisor for the latest contribution limits, eligible expenses, and any regulatory changes.

- Review HDHP Status Annually: Confirm that your health plan continues to meet the HDHP requirements for HSA eligibility, especially if your plan changes or renews.

- Evaluate Investment Performance: For invested HSAs, regularly check the performance of your chosen funds and rebalance your portfolio as needed to align with your financial goals.

- Keep Meticulous Records: Maintain detailed records of all qualified medical expenses, even if you pay out-of-pocket, to ensure you can justify tax-free withdrawals in the future.

- Educate Yourself: Continuously learn about new ways to leverage your HSA, from advanced investment strategies to understanding less common eligible expenses.

The power of Healthcare Savings Accounts in 2026 lies not just in their inherent benefits but in the informed and proactive management by account holders. By staying abreast of changes, optimizing contributions, and strategically investing, individuals can ensure their HSA remains a cornerstone of their financial planning, effectively managing medical expenses and building long-term wealth.

| Key Aspect | Brief Description |

|---|---|

| Triple Tax Advantage | Contributions are tax-deductible, funds grow tax-free, and qualified withdrawals are tax-free. |

| HDHP Requirement | Eligibility is tied to enrollment in a High Deductible Health Plan (HDHP) that meets IRS criteria. |

| Investment Potential | Funds can be invested for long-term, tax-free growth, acting as a powerful retirement savings tool. |

| Portability & Rollover | Funds belong to you, roll over year-to-year, and remain with you even if you change jobs or health plans. |

Frequently Asked Questions About HSAs in 2026

The IRS typically adjusts HSA contribution limits annually for inflation. While specific 2026 figures are usually released later in the year, it’s expected there will be separate limits for self-only coverage and family coverage under an HDHP, plus an additional catch-up contribution for those age 55 and over. Always check the latest IRS guidance for precise numbers.

Generally, no. To be eligible for an HSA, you must be covered by a High Deductible Health Plan (HDHP) and have no other health coverage, with some exceptions. These exceptions include specific types of coverage like dental, vision, long-term care, or disability insurance. Being enrolled in Medicare also disqualifies you from contributing.

One of the key benefits of an HSA is its portability. The funds in your HSA belong to you, not your employer or health plan. If you change jobs or switch to a non-HDHP, you can no longer contribute to the HSA, but you retain ownership of the existing funds and can continue to use them for qualified medical expenses.

Yes, you can generally use your HSA funds to pay for qualified medical expenses for yourself, your spouse, and your dependents, even if they are not covered by your High Deductible Health Plan. The key is that the individual must be a qualifying dependent for tax purposes, and the expense must be considered qualified by the IRS.

For those eligible, HSAs often offer more comprehensive benefits, including a triple tax advantage, tax-free growth through investments, and funds that roll over year-to-year. FSAs have a “use it or lose it” rule and lack investment options. However, FSAs don’t require an HDHP, making them suitable for individuals with traditional health plans.

Conclusion

Healthcare Savings Accounts (HSAs) in 2026 stand out as an indispensable tool for managing medical expenses and building long-term financial security. Their unique triple tax advantage—tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses—positions them as a powerful vehicle for both immediate healthcare needs and strategic retirement planning. By understanding eligibility, optimizing contributions, and embracing the investment potential, individuals can significantly enhance their financial well-being. Proactive management and staying informed about annual adjustments will ensure HSAs remain a cornerstone of smart financial strategy in an evolving healthcare landscape.

Contributions in 2025: Expert Guide")