COBRA Benefits 2026: Navigating Continued Health Coverage After Job Loss

COBRA Benefits in 2026 provide crucial temporary health insurance continuation options for eligible individuals and their families after job loss or other qualifying events, ensuring vital access to medical care.

Losing a job can be a profoundly unsettling experience, bringing with it a cascade of concerns, not least among them the daunting question of continued health coverage. In 2026, understanding your options, particularly regarding COBRA Benefits 2026: Navigating Continued Health Coverage After Job Loss, is more critical than ever. This guide aims to demystify the complexities surrounding COBRA, helping you make informed decisions during a challenging transition.

Understanding COBRA: The Basics for 2026

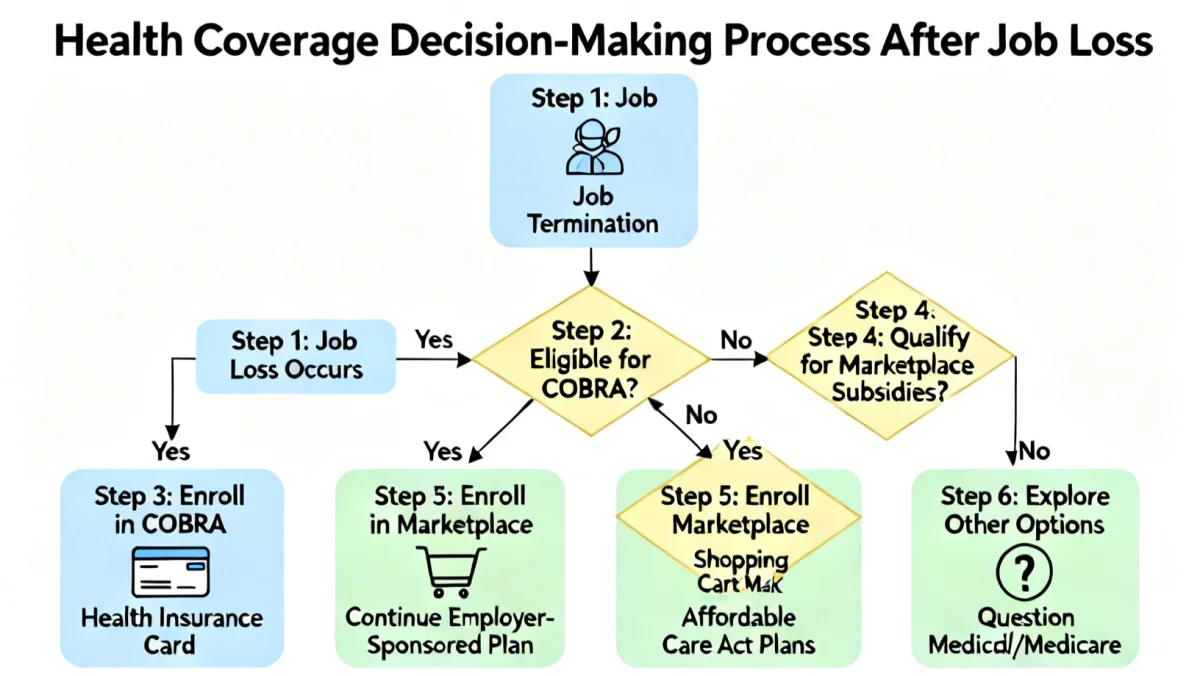

The Consolidated Omnibus Budget Reconciliation Act (COBRA) offers a vital safety net, allowing certain employees and their families to continue group health benefits provided by their employer for a limited period after job loss or other specific events. As we move into 2026, the fundamental principles of COBRA remain consistent, yet it’s essential to grasp the nuances that might impact your choices and costs.

COBRA is not a new health plan but rather a continuation of your existing employer-sponsored coverage. This means you retain the same network of doctors, hospitals, and benefits structure you had while employed. However, the key difference lies in who pays for it. When you elect COBRA, you typically pay the full premium, including the portion your former employer previously covered, plus a small administrative fee.

Eligibility Criteria for COBRA in 2026

To be eligible for COBRA in 2026, a few conditions must be met. These criteria ensure that COBRA is available to those who genuinely need it for a transitional period.

- Qualified Beneficiary: This includes employees, their spouses, and dependent children who were covered by the group health plan on the day before the qualifying event.

- Qualifying Event: Events such as voluntary or involuntary termination of employment (for reasons other than gross misconduct), reduction in hours, divorce or legal separation, death of the covered employee, or a child losing dependent status.

- Covered Plan: The employer’s health plan must be subject to COBRA, generally meaning it’s a private-sector employer with 20 or more employees or a state/local government employer.

It’s important to note that not all employers are subject to COBRA. Small employers (fewer than 20 employees) are usually exempt, though state continuation laws (often called “mini-COBRA” laws) might offer similar protections. Always verify your employer’s obligations.

The duration of COBRA coverage typically ranges from 18 to 36 months, depending on the qualifying event. For instance, job termination usually grants 18 months, while certain multiple qualifying events can extend it to 36 months. Understanding these durations is crucial for long-term planning.

Navigating the Costs of COBRA: What to Expect in 2026

One of the most significant considerations when electing COBRA Benefits 2026: Navigating Continued Health Coverage After Job Loss is the cost. Without employer contributions, the premiums can seem substantial. It’s vital to budget for these expenses and compare them with other available options.

COBRA premiums are calculated based on the total cost of the plan. This includes both the employer’s and employee’s share of the premium, plus an administrative fee of up to 2%. For many, this can translate to hundreds or even thousands of dollars per month, depending on the plan’s richness and the number of family members covered.

Strategies for Managing COBRA Costs

While COBRA can be expensive, there are ways to approach its costs strategically. Sometimes, the peace of mind offered by continuing familiar coverage, especially during ongoing medical treatments, outweighs the higher premium.

- Short-Term Solution: COBRA might be a good short-term bridge to new employment with benefits or until the next open enrollment period for a marketplace plan.

- High Healthcare Needs: If you or a family member has significant ongoing medical needs, continuing your current plan might be more cost-effective than starting a new plan with a different deductible or network.

- Compare with Marketplace Plans: Always compare COBRA premiums with plans available on the Health Insurance Marketplace (Healthcare.gov or state exchanges). You might qualify for subsidies based on your income, potentially making marketplace plans more affordable.

It’s also worth investigating if your former employer offers any severance packages that include a COBRA subsidy. While not common, some employers might offer to cover a portion of COBRA premiums for a limited time as part of a separation agreement. Always ask about this possibility.

The cost factor often drives individuals to explore alternatives, but for those who value continuity of care and a familiar provider network, COBRA remains a powerful option despite its price tag. Careful financial planning and comparison are key to making the best decision for your situation.

The Election Process: Activating Your COBRA Rights in 2026

Electing COBRA Benefits 2026: Navigating Continued Health Coverage After Job Loss involves specific steps and adherence to strict deadlines. Missing these deadlines can result in losing your right to COBRA coverage altogether, so understanding the timeline is paramount.

Once a qualifying event occurs, your employer has 30 days to notify the plan administrator. The plan administrator then has 14 days to provide you with an election notice. This notice outlines your COBRA rights, the cost of coverage, and how to elect it. You then have a 60-day election period from the date of the notice (or the date coverage would otherwise end, whichever is later) to decide whether to elect COBRA.

Key Steps in the COBRA Election Process

Following these steps meticulously will help ensure a smooth transition to COBRA coverage.

- Receive the Election Notice: This official document details your rights, costs, and the deadline for election. Read it thoroughly.

- Review Your Options: Compare COBRA with marketplace plans, spousal coverage, or short-term plans. Consider your health needs, financial situation, and provider preferences.

- Complete and Return Election Form: If you decide to elect COBRA, fill out the form accurately and return it by the specified deadline.

- Make Your First Premium Payment: You typically have 45 days from the date of your COBRA election to make your first premium payment. This payment covers the period from when your employer coverage ended. Subsequent payments are usually due monthly.

It’s important to remember that COBRA coverage is retroactive to the date your employer-sponsored coverage ended. This means that if you incur medical expenses during the election period before making your first payment, those expenses will be covered once you elect COBRA and pay the premiums. This retroactive coverage is a significant advantage, providing protection during the decision-making window.

Do not delay in reviewing your election notice and making a decision. Procrastination in this matter can have severe consequences for your health coverage and financial well-being.

Alternatives to COBRA: Exploring Other Health Coverage Options

While COBRA Benefits 2026: Navigating Continued Health Coverage After Job Loss offers a familiar bridge, it’s not always the most suitable or affordable option. Exploring alternatives is a crucial step in securing your health coverage after a job transition.

The Health Insurance Marketplace, established under the Affordable Care Act (ACA), is a primary alternative. Job loss is a qualifying life event that triggers a Special Enrollment Period (SEP), allowing you to enroll in a new plan outside of the annual open enrollment. Depending on your income, you might be eligible for premium tax credits and cost-sharing reductions, significantly lowering your monthly premiums and out-of-pocket costs.

Other Viable Health Coverage Pathways

Beyond the Marketplace, several other options might be available, depending on your circumstances.

- Spousal Coverage: If your spouse has employer-sponsored health insurance, job loss often qualifies you for a Special Enrollment Period to join their plan. This can be a cost-effective solution if their plan is affordable and meets your needs.

- Medicaid Expansion: In states that have expanded Medicaid, you might qualify for low-cost or free health coverage based on your income. Eligibility thresholds vary by state.

- Short-Term Health Insurance: These plans offer temporary coverage, often at a lower premium than COBRA. However, they typically don’t cover pre-existing conditions, may not cover essential health benefits, and are not subject to ACA consumer protections. They are generally not recommended as a long-term solution.

- Direct Enrollment with Insurers: Some insurers offer plans directly outside the Marketplace. While you won’t qualify for subsidies this way, it might be an option if you prefer a specific plan or insurer.

Each alternative comes with its own set of advantages and disadvantages regarding cost, coverage, and network. It’s advisable to get quotes from multiple sources and carefully compare benefits, deductibles, and out-of-pocket maximums before making a decision. The goal is to find coverage that aligns with your health needs and financial capacity.

Strategic Considerations for COBRA in 2026

Making an informed decision about COBRA Benefits 2026: Navigating Continued Health Coverage After Job Loss requires a strategic approach. It’s not just about electing coverage; it’s about understanding how it fits into your broader financial and health planning.

One key consideration is the “COBRA gap.” You have 60 days to elect COBRA, and coverage is retroactive. This means you could potentially wait until day 59 to elect and pay for COBRA, effectively giving you nearly two months of “free” coverage in the interim, knowing you can activate it if a major medical event occurs. However, this strategy carries risk: if you don’t elect COBRA within the 60 days, you lose your rights entirely.

Long-Term Planning and Future Coverage

Consider your long-term health coverage strategy when evaluating COBRA. Is your job search likely to be short, leading to new employer-sponsored benefits? Or do you anticipate a longer period without employer coverage?

- New Employer Benefits: If you expect to secure new employment quickly, COBRA might serve as a temporary bridge, allowing you to maintain continuity of care without having to change doctors or plans.

- Retirement Planning: For those nearing retirement, COBRA can bridge the gap until Medicare eligibility. However, other options like early retirement plans or ACA marketplace plans should also be evaluated.

- Family Needs: If you have family members with chronic conditions or ongoing medical needs, continuity of care through COBRA might be invaluable, even at a higher cost.

Another strategic point is understanding the interaction between COBRA and the Health Insurance Marketplace. If you elect COBRA, you generally cannot switch to a Marketplace plan with subsidies until the next Open Enrollment Period, unless you exhaust your COBRA coverage or stop paying premiums (which is considered a loss of coverage). However, if you *don’t* elect COBRA initially, you can immediately enroll in a Marketplace plan via a Special Enrollment Period.

Careful consideration of these strategic points, along with your personal health and financial situation, will guide you toward the most appropriate health coverage decision after job loss.

The Impact of Legislation and 2026 Trends on COBRA

The landscape of health benefits is always evolving, and while the core tenets of COBRA remain stable, legislative changes and emerging trends can influence its practical application. For COBRA Benefits 2026: Navigating Continued Health Coverage After Job Loss, staying informed about potential shifts is important.

While no major overhauls to COBRA are anticipated for 2026, smaller legislative adjustments or regulatory interpretations could occur. For instance, temporary subsidies for COBRA, like those seen during the COVID-19 pandemic, are not currently on the horizon for 2026, so individuals should generally expect to pay full premiums.

Future Outlook and Considerations

Beyond direct legislation, broader trends in healthcare and employment can indirectly affect COBRA’s utility.

- Rising Healthcare Costs: The ongoing trend of increasing healthcare costs means COBRA premiums are likely to remain high. This reinforces the need to carefully compare COBRA with subsidized Marketplace plans.

- Remote Work and Gig Economy: The rise of remote work and the gig economy may lead to different benefit structures, potentially affecting who is offered traditional employer-sponsored plans subject to COBRA.

- Technological Advancements: Digital tools and platforms continue to improve, making it easier to compare health plans, manage enrollment, and access information about COBRA and other options.

It’s always advisable to consult official government resources, such as the Department of Labor (DOL) and the Department of Health and Human Services (HHS), for the most up-to-date information regarding COBRA and health insurance regulations. These agencies provide reliable guidance on your rights and responsibilities.

Staying informed about these trends and potential legislative changes will empower you to make the most advantageous decisions regarding your health coverage in 2026 and beyond. Proactive research and consultation with benefits specialists can make a significant difference during times of transition.

| Key Aspect | Brief Description |

|---|---|

| Eligibility | Applies to employees, spouses, and dependents after qualifying events (e.g., job loss) from employers with 20+ staff. |

| Cost | Full premium (employer + employee share) plus up to 2% administrative fee, making it often expensive. |

| Election Period | 60 days from notice or loss of coverage to elect; 45 days for first payment. |

| Alternatives | Health Insurance Marketplace (with potential subsidies), spousal coverage, Medicaid, or short-term plans. |

Frequently Asked Questions About COBRA Benefits 2026

The main benefit of COBRA is the continuation of your existing employer-sponsored health plan. This means you keep your doctors, hospital networks, and benefit structure, providing seamless care during a transition period, especially for those with ongoing medical needs.

The duration of COBRA coverage typically depends on the qualifying event. For job termination, it’s generally 18 months. Other events, such as a spouse’s divorce or a child aging out of dependent status, can extend coverage up to 36 months in specific circumstances.

Not always. While COBRA offers continuity, it can be expensive. It’s crucial to compare COBRA costs and benefits with other alternatives like Health Insurance Marketplace plans, which may offer subsidies, or spousal coverage, to find the most cost-effective and suitable plan for your needs.

If you miss the 60-day deadline to elect COBRA, you generally lose your right to enroll in COBRA coverage. This is why it’s critical to act promptly upon receiving your election notice and carefully consider all your available health insurance options.

Yes, you can. While electing COBRA typically prevents you from immediately getting a Marketplace Special Enrollment Period, you can switch to a Marketplace plan during its annual Open Enrollment Period or if your COBRA coverage ends (e.g., you exhaust its duration or stop paying premiums).

Conclusion

Navigating the complexities of health coverage after job loss demands careful consideration, and COBRA Benefits 2026: Navigating Continued Health Coverage After Job Loss stands as a critical option for many. While its cost can be a deterrent, the ability to maintain familiar care and provider networks offers invaluable peace of mind during a period of significant change. By understanding eligibility, costs, the election process, and viable alternatives, individuals can make informed decisions that safeguard their health and financial well-being. Proactive research and a clear understanding of your personal circumstances are paramount to securing the best possible health coverage in 2026.